The flaky case for buying the dip

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Either the mighty US mom-and-pop investor base knows something we don’t, or it’s heading for a bruising.

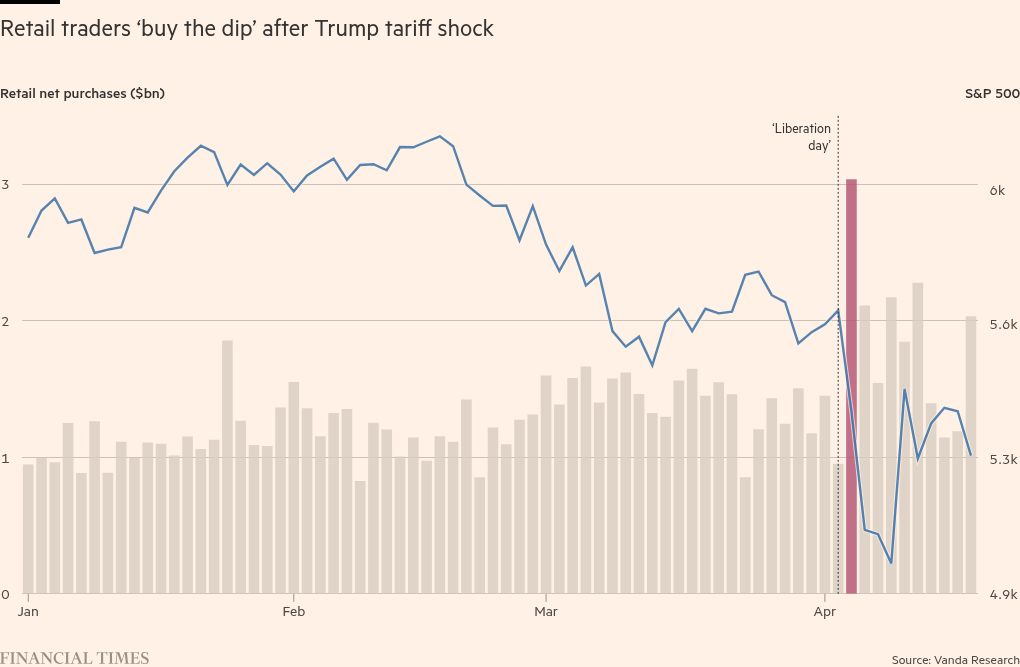

Right now, the amateurs are sitting pretty. Domestic retail investors were, by all accounts, conspicuously active buyers of US stocks in the initial firestorm kicked off by Donald Trump’s so-called “reciprocal” tariffs announcement at the start of this month.

As stocks indices plunged, purchases from this group were, as Vanda Research puts it, “historic”. Fair play to them. It was a brave call, but from the very lowest point on April 7, the US S&P 500 is still up by 9 per cent.

In recent years, retail punters have been an important market segment for professional investors to watch. They were swift to buy the (much larger) dip after the Covid shock five years ago, jumping in when many institutional investors were still too nervous, and they were absolutely right. It is worth thinking about what drives them.

Logic dictates that one reason is a large number of have-a-go investors in the US voted for Trump, and quite possibly believe his argument that massive import taxes are poised to rekindle jobs in the country’s manufacturing sector.

However, muscle memory is a powerful thing. The past 65 years tell us that US stocks reliably go up, in roughly twice as many years as they go down. Positive runs are much more powerful and longer lasting than bad patches.

Even for more heavy-hitting institutional investors, the rationale for buying now, when US stocks are down by some 10 per cent so far this year, is incredibly strong, if we are playing by the usual market rule of zigging when the world zags. (Note the “if”.)

The mood among fund managers is absolutely dire. Bank of America’s regular monthly survey of institutional investors, released this week, is pretty apocalyptic — the fifth most miserable reading in its quarter-century history. Growth expectations are at 30-year lows, with almost half now expecting a hard landing in the US. A record number of respondents intend to cut exposure to US stocks.

When institutional investors turn that miserable that fast, your inner contrarian would normally tell you to be brave like US retail investors and jump in.

Some of the woe-is-me wailing at the sky from professional fund managers may also be a little performative. “Today we’re hearing a lot that we’ll never go back,” said Michael Kelly, head of multi-asset at PineBridge Investments. “But I know finance people, and they’ll do whatever makes sense in future. Wall Street people will go where the cheese is.”

A hint of the notion that the pain has gone too far is also evident in US government bond markets, typically the territory of the professionals. Treasuries are, in many maturities, strikingly weak, despite the three to four interest rate cuts investors now anticipate for the rest of this year that would normally waft bond prices higher.

Mike Riddell, a bond fund manager at Fidelity International, said he had been running smaller allocations to Treasuries than normal, but “we have been scaling into it now”, he said, adding that he’s “getting to the point” where they are cheap enough to pique his interest.

So, pack in your caveats as you see fit. On paper, in theory, on average, based on historical precedent and if the usual rules apply, the present moment is a once-in-a-generation opportunity to snaffle up US assets on the cheap.

And yet the rush to do that is just not there. The consensus among the pros is that the tariffs policy itself is a mess. One moment, commerce secretary Howard Lutnick is on US television telling the world about the administration’s grand vision of “millions” of Americans fixing tiny screws in to iPhones as part of a new golden age for American craftsmanship, and a week later, his boss decides to exempt smartphones from some of the tariffs altogether. In any case, it takes years to bring sophisticated manufacturing back home, and the next US president could scrap the import taxes entirely. In that environment, few sane US company executives would crank up domestic manufacturing as Trump hopes.

Meanwhile, the president is busily launching blunt broadsides against Federal Reserve chair Jay Powell and, the icing on the cake — the US’s crucial tech sector took a massive hit this week after chips giant Nvidia said it would take a multibillion-dollar earnings hit from new export restrictions to China. The Philadelphia semiconductor index is down by 22 per cent this year.

Uncertainty in markets is nothing new. It is the whole point. It is why certain assets pay out returns to those brave enough to buy them. But it has a whole new flavour now. An orange flavour.

Record-breaking gold prices, a soaring Swiss franc and a massive jump in German government bonds are all a clear sign that professional investors are deeply spooked, and anticipating the next wave of pain. If the retail dip buyers are right again, this will have been a heroic call on their part, but the odds are heavily stacked against them. My hunch is that the beatings will continue until morale improves.

katie.martin@ft.com