Brexit lessons for Trump’s trade war

In his latest display of fealty before Donald Trump, US Treasury secretary Scott Bessent described the president’s U-turns over tariffs as a deliberate act in creating “strategic uncertainty”. According to Bessent, certainty is over-rated and waywardness brings leverage to negotiations that will generate the best trade deals for the US.

This confident talk reminded me of Brexit, where former prime minister Boris Johnson promised the UK would get a “great deal” from the EU, while his Leave-campaigning sidekick Michael Gove insisted that Britain would “hold all the cards” in any negotiation.

Brexiters thought the UK goods trade deficit gave them a winning hand and that the trade barriers that Britain wanted to erect with the EU would benefit Britain’s exports. I know — it did not make any sense even at the time.

Normally in economics, we treat bygones as bygones. You need to look forward and not ponder past decisions that cannot be undone. But on this occasion, where there are similarities, it is worth looking at how much milk was spilled by Brexit.

Between the 2016 referendum and the EU-UK Trade and Cooperation Agreement coming into force on January 1 2021, the UK created its own strategic uncertainty with multiple ambitions, tactics and prime ministers. Business investment stalled, sterling fell and inflation exceeded that of other countries. Before 2016, Brexiters complained that the UK was economically “shackled to a corpse”, but the UK’s previously superior growth performance compared with the EU soon disappeared.

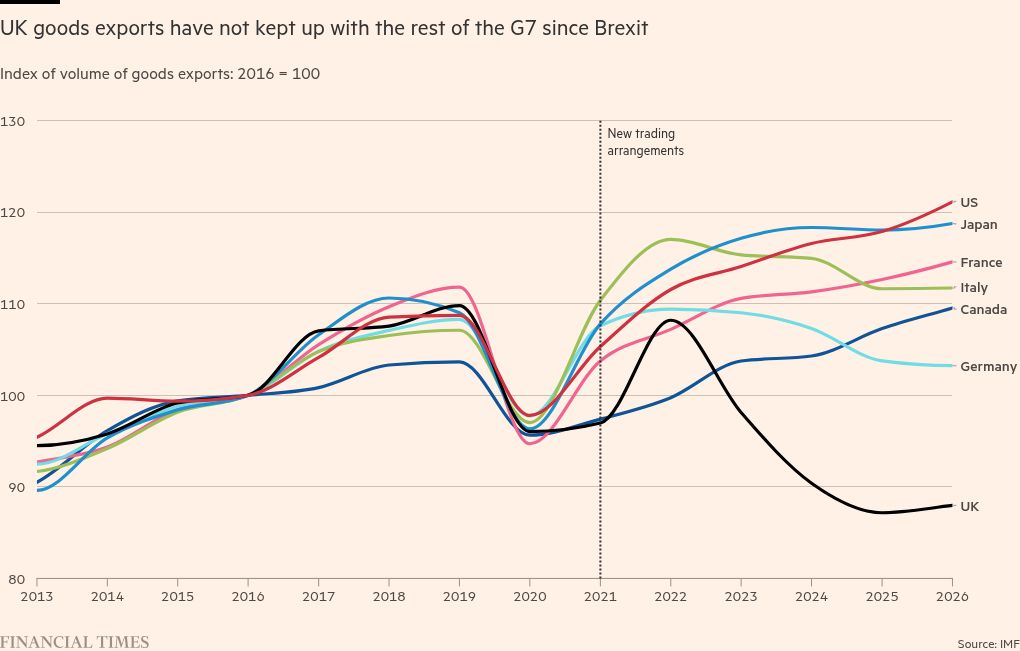

Those losses have not been recovered. Since the 2021 free trade deal with the EU brought the certainty of higher trade barriers to Britain, the diminished flow of goods across the Channel has been most notable. The quantity of UK goods exports are lower now than in 2016 or 2021 and Britain is the only country in the G7 that has this record.

Sure, it’s possible to explain away aspects of this shocking performance. Some of it comes from fuels, which is more likely to reflect declining North Sea oil production rather than Brexit. And Britain’s goods export performance with non-EU countries is about as poor as it is with the EU, which suggests a problem with the UK as a whole. Services exports have done OK.

But it is impossible to construct a coherent argument that Brexit has benefited the UK economy. Britain’s diminished role feeds vigorous debate on exactly how much damage has been done and whether it is wiser to suck up to the US or the EU in the hope of being thrown some scraps from one of their tables.

Mark Carney, who was intimately involved in the Brexit wrangles as Bank of England governor and now must negotiate with Trump as Canadian prime minister, put it well at the weekend, saying the lessons of Brexit are now being applied to the US. “When you break off, or substantially rupture trading relationships with your major trading partners . . . you end up with slower growth, higher inflation, higher interest rates, volatility, weaker currency and a weaker economy,” he said.

It was painful to live through this experience in Britain. Modern capitalist economies are extremely resilient, so there is rarely that cathartic moment where the whole country realises it has made a terrible mistake and steps away from the edge. So there is little doubt that the Trump administration will continue to peddle fantasies about its strategic brilliance, while fighting internally over day-to-day tactics and trade deals that at best recreate the advantages that the US already had. Trade is relatively unimportant to the US economy, and it can withstand a lot of this nonsense without necessarily crumbling.

But a stagflationary shock is just that. When it comes to a reckoning in some years’ time, the US economy will be weaker and its standing in the world diminished. Brexit teaches you that.