Private capital: growth opportunity or minefield?

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

As proofs of concept go, the St James’s Place Diversified Assets fund, backed by US-based KKR and available to clients of the UK wealth manager since 2018, has not been a storming success.

The fund, which specialises in a mix of private capital investments, has returned just 0.6 per cent over the past year. Listed equities on the FTSE 100 have generated a total return of more than 8 per cent over the same period; even cash could have made you 5 per cent. The underperformance has persisted over longer periods, too.

This is worth noting, as the UK political and pensions establishment enthuses about private capital. Last week, Chancellor Rachel Reeves unveiled a Mansion House Accord with 17 of the UK’s largest pension fund managers. Under the terms of the voluntary pact, 10 per cent of the default funds of defined contribution pension schemes managed by the signatories are to be allocated to private markets by the end of the decade, compared with next to nothing today. Reeves also has left open the possibility of mandating the asset allocation, if the voluntary pledge doesn’t look like it’s working.

At the same time in the US, asset managers are striking partnerships to give mainstream retail investors easier access to private capital. Vanguard and Wellington have teamed up with Blackstone while Capital Group has partnered with KKR.

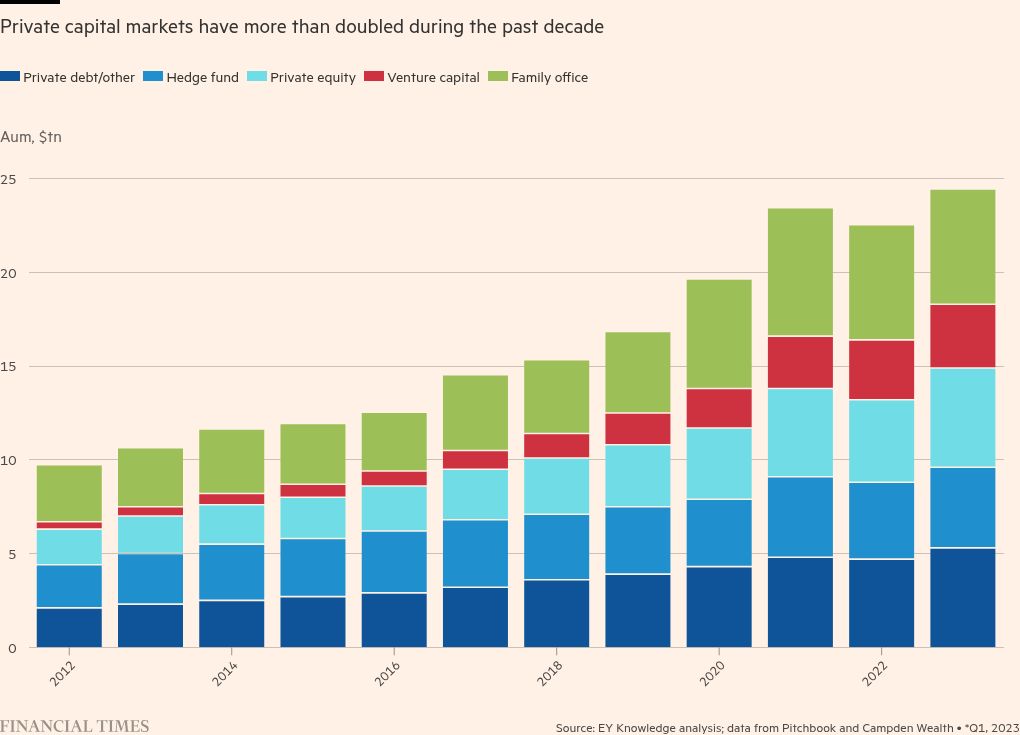

Why the obsession with private markets? Well, notwithstanding the poor record of that Diversified Assets fund, there is evidence of pretty consistent outperformance across the industry. Over decades, private equity has typically delivered annual so-called internal rates of return in the teens, according to a 2022 academic paper; the S&P 500 total return has averaged about 10 per cent. (KKR itself has generated annual net IRRs in its private equity and infrastructure private client funds of up to 12 per cent and 14 per cent, respectively.) The private capital market has more than doubled in size in a decade and now boasts close to $25tn of assets under management.

That kind of record, plus the bald fact that private company structures are gaining in popularity compared with listed ones, has left investors and policymakers alike with a growing fear of missing out. But in the context of both the UK pensions push and the US retail investor initiatives, the picture is clouded by many complicating factors and resulting risks.

First, policymakers may be conflicted. Wanting to fuel economic growth by encouraging certain kinds of investment is valid. Pressuring pension money into, for example, hard-to-finance, and potentially high-risk, infrastructure projects is not.

Second, consider the self-interest of pensions managers who could benefit from their slice of larger fees. (A typical private capital fund would charge an annual fee of up to 2 per cent, sometimes with arcane performance charges on top — a far cry from the total expense ratio of as little as 0.1 per cent on a public equities tracker.)

Third, the private capital industry itself is hungry for a supply of new end investors. Interest rates are now higher than they have been for much of the past 20 years, making the debt funding that private capital relies on more expensive. That has meant returns have been on the decline. Exiting investments has become harder, too, as initial public offerings struggle in moribund markets for equity issuance. These and other factors mean the private equity industry is finding it harder to raise new funds from their traditional institutional backers — sovereign wealth funds, university endowments and hyperscaled pension funds, like those in Canada and Australia. So winning over new funds, like DC providers in the UK, or retail investors in the US, is a good diversification strategy.

Retail investors may be seen by unscrupulous financiers as “dumb money”. In some recent transactions, retail funds that take stakes in existing buyout funds have been paying higher prices than other bidders, such is the surge in the supply of retail money. Attempts to make retail funds more palatable to mainstream investors, by offsetting the inherent illiquidity of many private capital assets with more liquid ones, may also undermine performance. SJP’s KKR fund, which offers daily liquidity, currently holds 30 per cent cash. (SJP is now reviewing its private capital strategy, insiders say.)

For policymakers and investors alike, there is one message to be drawn from all of this: private capital may present an enticing growth opportunity, but is not the simple panacea they might like to imagine.

patrick.jenkins@ft.com