Trade, tech and Treasuries: China holds cards in US tariff stand-off

The US and China are locked in a dangerous trade stand-off, with the world’s two largest economies trading tit-for-tat blows as Donald Trump demands Beijing seek a deal from his administration.

China relies on the US as an almost irreplaceable market for its manufactured goods, but experts warn that Washington should not underestimate Beijing’s capacity to resist Trump’s coercive tactics.

The combination of centralised political control, increasingly diversified export markets and its virtual stranglehold on some strategically vital materials, including rare earth metals, gives Beijing plenty of negotiating power. The question is how far it can use its leverage without suffering even more damage itself.

Trade power

China had a trade surplus of almost $300bn with the US last year, with about 15 per cent of its total exports heading into the US. Trump’s tariffs of 145 per cent would inflict significant pain on Beijing.

But international economists said this overlooks one crucial fact: China can replace its imports from the US more easily than the other way around.

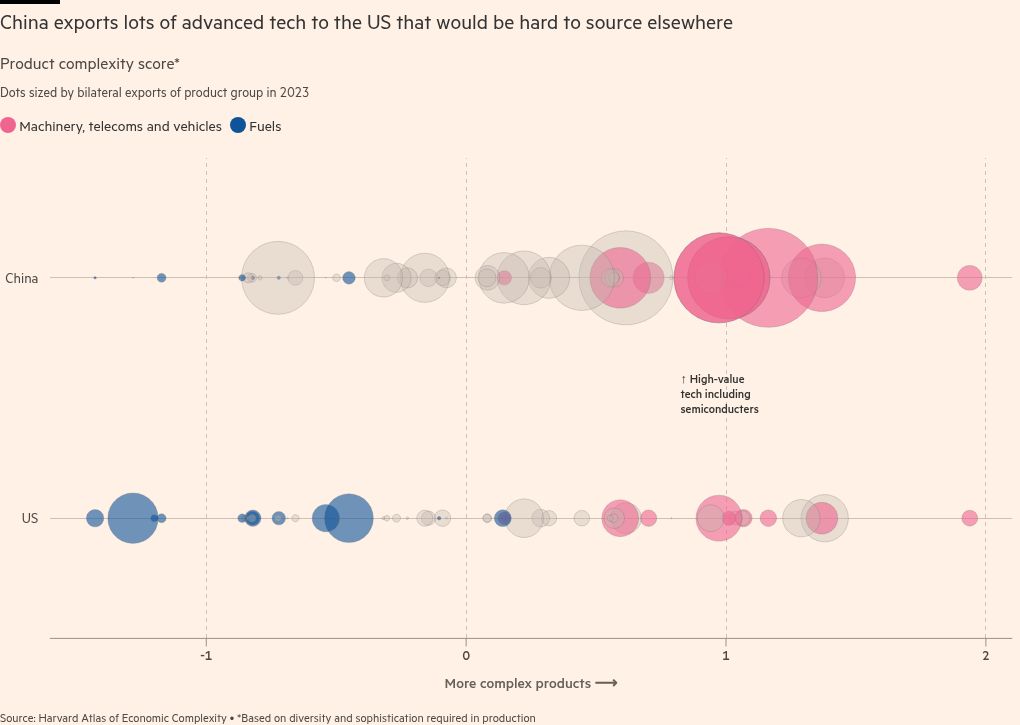

US goods exports to China are heavily focused on agriculture — such as soyabeans, cotton, beef and poultry — and so are low value-added. Many US imports from China — electronics, machinery and some processed minerals — are the opposite.

Marta Bengoa, professor of international economics at City University of New York, said that while the US and China remained heavily interdependent in trade, this meant the ultimate balance of risk was on the US side.

“US dependence on China is higher, because China can source agricultural products from elsewhere more easily than the US can replace electronics and machinery,” she said. “Beijing is already buying up soyabeans from Brazil, for example, so in the end China has a bit more leverage”.

The depreciating dollar has also made it more expensive for the US to import goods.

The pain of a trade war will still be felt in China, which imports higher-end products from the US, including aircraft parts, pharmaceuticals and semiconductors — although Washington has sought to restrict access to chips in recent years. Many American businesses are embedded in supply chains on the ground in the country.

Goldman Sachs analysts estimated that 10mn-20mn workers in China may be exposed to US-bound exports. “The combination of extremely high US tariffs, sharply declining exports to the US and a slowing global economy is expected to generate substantial pressures on the Chinese economy and labour market,” they wrote last week.

Strategic ‘backdoor’

Since Washington imposed sectoral tariffs on steel, aluminium, solar panels and washing machines in 2018 and 2019 during Trump’s first term, China has tried to reduce its reliance on exports to US consumers. Its share of US imports has fallen from 21 per cent in 2016 to 13.4 per cent last year, according to US government data, slashing Beijing’s trade exposure.

At the same time, Chinese production capacity has been rerouted through south-east Asian countries such as Vietnam and Cambodia, where Chinese manufacturers took advantage of cheaper labour and reduced exposure to US tariffs. Exports to Vietnam soared 17 per cent in March, data released this week showed.

How determined Trump is to shut that “back door” for Chinese exports remains to be seen. Vietnam, which now runs a $124bn trade surplus with the US, has been threatened with a “reciprocal” 46 per cent tariff — though this was suspended for 90 days.

Alicia García Herrero, chief economist for Asia-Pacific at French investment bank Natixis and a senior fellow at the Bruegel think-tank, said the pause provided some breathing space. “Essentially that gives both sides 90 days of leeway in order to figure things out.”

But even if there was a hard cessation of Chinese exports, García Herrero said the impact would not be catastrophic on China’s sprawling economy. The country’s GDP grew 5 per cent last cent last year, 1.5 percentage points of which was derived from its near-$1tn global trade surplus.

“China is a humungous economy that is resilient,” she said.

But analysts also warned that Chinese attempts to redirect excess capacity to alternative markets including the EU, India and countries across the global south could invite blowback.

“Because of the surplus of goods that China is going to be looking to offload, I would expect other countries to react to the potential deluge,” said Alex Capri, senior lecturer in the Business School at the National University of Singapore.

Financial holdings

China enjoys further leverage from the large pile of US government debt it has accumulated, which it could in theory sell to reduce its exposure. That in turn could raise concerns about the attractiveness of US assets and precipitate further declines in value of the dollar and US government debt.

Zerlina Zeng, head of Asia credit strategy at CreditSights, noted that a sell-off in Treasuries would also hit China, given the size of its holdings.

“That said, we expect China to continue diversifying its US dollar-denominated reserves into other currencies as a long-term allocation goal,” she said.

Critical minerals

The US is also reliant on China for many rare earth metals essential for modern manufacturing, such as in electric vehicle batteries. Beijing controls more than two-thirds of global rare earth production and more than 90 per cent of processing capacity — a critical point of leverage.

Trump excluded critical minerals from his first round of “reciprocal” tariffs in an acknowledgment of US vulnerabilities. But such waivers may not be enough to avoid a supply crunch if China digs in.

China placed export controls on seven more rare earth elements last week, including dysprosium and terbium, which are essential ingredients in products such as jet engines and EVs.

Autocracy over democracy

While China’s ruling Communist party is not immune to swings in public opinion, it is less reactive to pressure than the White House, which has already been forced to respond to turmoil in the bond and stock markets and the threat of higher prices.

Alfredo Montufar-Helu, head of the China Center at the Conference Board think-tank in New York, noted that Beijing — despite contending with challenges of its own — was entering the trade stand-off with a greater capacity to stimulate its economy in the event of a slowdown.

It also has more levers to manipulate its domestic market, which Chinese authorities watch as an indicator of social stability and economic sentiment. Beijing has intervened heavily in the market in recent weeks, with the “national team” of state institutions driving co-ordinated action to support share prices.

But China’s government is also highly sensitive to displays of public discontent. In late 2022, it lifted its three-year Covid-19 restrictions shortly after protests emerged in major cities.

“Just from the market reaction, I’d say the US at the moment [is hurting more],” added Julian Evans-Pritchard, chief China economist at Capital Economics. “The US is under more pressure to try to come to the table and negotiate.”

But the first tremors of a trade war — such as delayed sailings from China’s vast ports — have yet to feed into open dissatisfaction in China’s southern manufacturing provinces.

“I haven’t met a single person, even manufacturers directly impacted by the tariff, who blames Beijing,” said one foreign manufacturer based in Guangdong province. “The mood that I’ve seen is a kind of defiance. I think the way the government is playing it is about national pride now.”

Additional reporting by Chan Ho-him in Hong Kong; data visualisation by Alan Smith in London