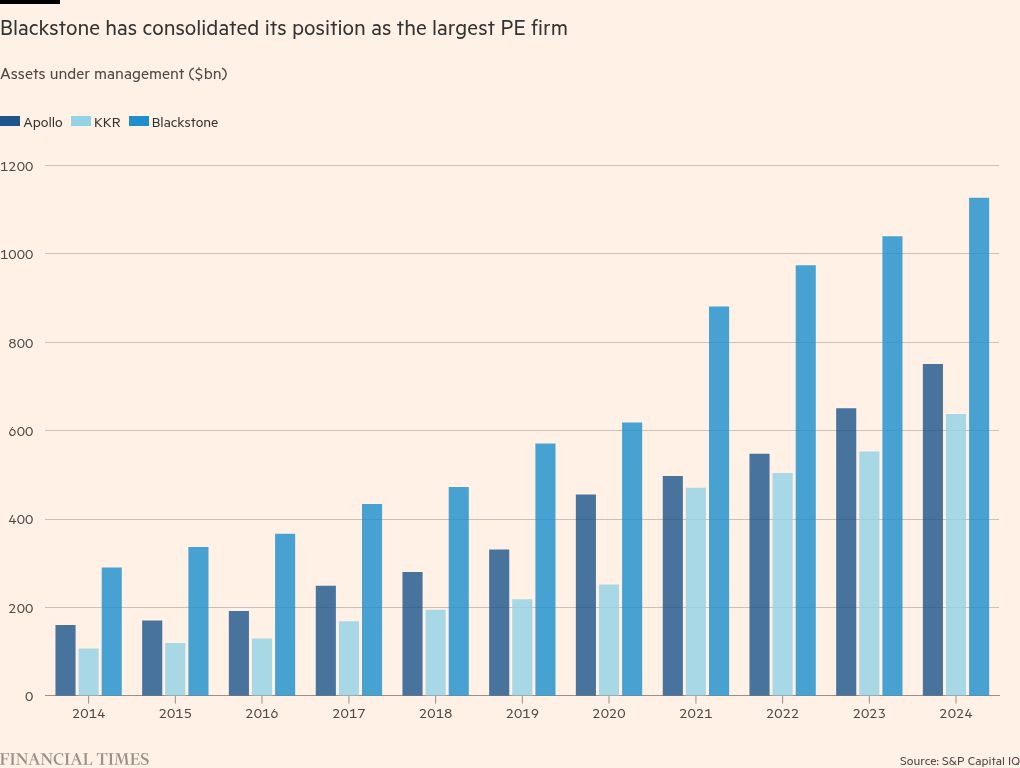

How Blackstone and its biggest rivals are drifting apart

By the standards of Wall Street earnings calls, where executives are typically wary of commenting on politics or the businesses of their rivals, it was quite a barb.

“For some, ‘capital-light’ has become code for ‘heads we win, tails we win and hopefully our clients do OK’,” said Jim Zelter, president of Apollo Global Management, referring to a private equity business model that focuses mostly on running other people’s money in return for a fee.

It was a thinly veiled jibe at the company’s biggest rival, Blackstone, and its co-founder Stephen Schwarzman, who had earlier told his own shareholders that the $1tn-plus private investment group he had built was “an asset-light manager of third-party capital with minimal net debt and no insurance liabilities”. He added that this model was lower risk and gave the group “enormous flexibility to respond to changing conditions”.

The verbal jousting highlights a growing divergence in approach between the three leading groups in the $13tn private capital industry. It comes as private equity appears to be losing the momentum it enjoyed for decades, with many groups finding it harder to raise new money or struggling to exit existing investments.

Competitors that had long followed similar financial models have responded by creating very different structures that could be special weapons during tumultuous markets — or lead to unforeseen vulnerabilities.

Blackstone has opted to stick with the traditional approach of managing investors’ money for a fee, which is lower risk but requires it to continually source more funds to manage.

Apollo has harnessed its asset portfolio to the steady stream of income produced by an insurance operation — an approach that provides it with long-term capital, but introduces leverage and makes its finances more akin to those of a bank.

Buyouts pioneer KKR has also acquired a large insurer and embraced a strategy similar to the one employed by Warren Buffett at Berkshire Hathaway. It has invested in a growing portfolio of private companies whose asset values and earnings compound within the group, but at the risk of painful writedowns if the investee companies do not perform as expected.

“Everybody’s doing the same thing on the front of the house,” says an executive of one large private capital group, referring to the everyday dealmaking of large private capital groups. “It’s the back of the house where the differences emerge . . . and these are pretty radically different businesses.”

For much of the decades-long ascent of the private capital industry, its biggest players moved in lockstep. Blackstone, Apollo and KKR all trace their rise to the first wave of leveraged buyouts, from the late 1970s to the early 1990s.

KKR, founded in 1976 by Henry Kravis, George Roberts and the late Jerome Kohlberg, was the first to make large debt-funded corporate takeovers mainstream. Its success prompted two top bankers of that era, Schwarzman and the late Pete Peterson to ultimately focus Blackstone — founded in 1985 — away from advising corporate mergers and towards constructing large buyouts itself.

Apollo co-founders Leon Black, Marc Rowan and Josh Harris all worked for Michael Milken, the so-called junk bond king who pioneered the use of subinvestment grade debt to finance leveraged takeovers. In the early 1990s, after Milken’s Drexel Burnham Lambert investment bank collapsed, the trio snapped up Executive Life, an insurer reeling from its holding of junk bonds sold by Drexel years earlier. Their bet that the bonds would quickly recover paid off, leading to the creation of Apollo.

From the 1990s to the mid-2000s, the three groups followed the same playbook: attracting tens of billions in new assets, mostly on the back of high returns from private equity takeovers. Their large windfalls in the early 2000s contrasted with the losses suffered by venture capital firms and mutual funds during the dotcom bust, and earned them a reputation as some of Wall Street’s smartest managers.

Blackstone led a drive to diversify its operations beyond buyouts and was the first to float in 2007, with KKR and Apollo following as markets recovered from the global financial crisis. After lacklustre early performance on public markets, their stock values soared as they grew increasingly diversified from originating private loans and investing in property and infrastructure. Starting in 2017, they all also restructured their operations so their shares could be included in the S&P 500 index.

Only after 2020 did their approaches start to dramatically alter. “It is post-pandemic where you are seeing the divergence and separation of the three business models more clearly,” says Michael Cyprys, an analyst at Morgan Stanley.

Blackstone’s approach means it is not directly on the hook for investors’ losses if its deals go sour or if markets head south. “I think the model is very well designed for periods of stress,” said Jonathan Gray, Schwarzman’s heir apparent, on the same earnings call. “[We] can weather a storm.”

It has also left the group with a net surplus of more than $7bn in cash and investments over debt. But critics say it means Blackstone has to keep coming back to investors for more funds, even if market conditions are not conducive to raising money or investing it.

By contrast, Apollo has $395bn of assets on its balance sheet — mostly arising from the life insurance contracts its insurance business has promised to millions of retirement savers — backed by just $32bn of equity. The resulting asset leverage ratio of 12.2 times is comparable to banks such as JPMorgan, although rating agencies treat Apollo’s insurer and its asset manager as separate entities, with the former carrying around 10 times.

Apollo and KKR’s embrace of insurance assets and leverage stems from their belief that lucrative deals will be in increasingly short supply, leaving them needing to squeeze more from each investment they make as owners alongside their clients.

Blackstone has balked at owning an insurer over fears that its investment business would have to cover policyholder losses in the event of a market collapse, and the more onerous regulation that writing insurance brings. It also contends that a fee-based model is more transparent and predictable and that its shares will command a higher valuation. It allows Blackstone to pay out most of its profits in dividends, with Schwarzman having received billions in such payments.

“Done right, you should get more growth in a balance sheet heavy strategy,” says Cyprys.

“But investors historically have tended to favour capital-light business models from a valuation standpoint. You don’t have that principal risk and exposure.”

Apollo’s decision to combine its investing activity with an insurance operation was the brainchild of Rowan.

In 2009, he established Athene, named after the Greek goddess of wisdom, and began buying large tranches of policies for Apollo’s investors to manage. Athene paid fees to Apollo to uncover more complex investments that could earn solid yields in an environment of rock-bottom interest rates.

Apollo made early profits for Athene by purchasing distressed mortgages that quickly recovered. The group gradually increased its stake in Athene, which turned to originating loans to generate profits as debt markets recovered from the crisis. The fast-growing insurer floated in 2016.

But stock market investors never warmed to the opaque fee arrangements and when Rowan became chief executive in 2021 — after Black became enmeshed in the Jeffrey Epstein scandal — his first big move was to merge Athene into Apollo.

Since then, Athene has roughly doubled its assets as Rowan builds what is in effect a bank, using longer-term insurance capital rather than flightier bank deposits to lend to investment-grade groups such as AT&T, AB InBev and Sony Music.

Apollo is on track to originate about a quarter of a trillion dollars in new loans this year — a figure that rivals megabanks such as Citigroup. Lending to commercial borrowers, rather than simply parking the premium income in more liquid but low-return assets, also allows it to generate a profitable spread over the largely fixed payouts that Athene has to make to its customers throughout their policies.

Apollo generates fees of about 1.4 per cent for each asset it originates, against just 0.4 per cent if it were to manage money for Athene on an arm’s-length basis. Rowan sees this as a safer model than funding low-rated buyout loans.

“If you believe that assets are in short supply you should want within a range to make as much money on each asset as possible,” he told shareholders last year. “You should want a fee, but you should also want a piece of the principal activity. That way, if I want to double my business, I don’t have to double the number of assets.”

But the model still comes with banklike risks. Athene has promised fixed returns on hundreds of billions of dollars in annuities policies that could come under pressure if interest rates drop or policyholders choose to terminate their contracts — and these assets now sit on the merged company’s balance sheet.

Last year Apollo arranged a $15bn hedge to protect against falling rates, and said that this and a deliberate exposure to shorter-term assets negate most of its interest-rate risk.

“Balance sheet intensity tends to have a more adverse mark to market risk,” notes William Katz, an analyst at TD Cowen.

Although it has nailed its colours to the mast of a fee-based model, Blackstone did consider the insurance option. In 2020, it considered buying a large minority stake in Global Atlantic alongside one of its largest investors.

The transaction would have given Blackstone control over its own insurer, rather than the asset management contracts it ultimately agreed with third-party insurers. But KKR — a group then roughly half Blackstone’s size by assets and market value — won the day thanks to its superior cash reserves, buying a majority stake in the insurer for more than $4bn.

It was a vivid demonstration of KKR’s conglomerate approach, under which co-chief executives Scott Nuttall and Joe Bae use retained profits to invest in majority-controlled businesses to hold for the long term.

Global Atlantic’s assets and book value have more than doubled in just five years, making the deal a big winner. KKR has told investors that its strategic investments in 19 companies are set to pay out over $1bn in dividends annually by the end of the decade, creating a third earnings stream to supplement the fees it receives for managing money for institutions and the spread profits earned by Global Atlantic.

They also spread management risk. “Once companies, especially financial services companies, get to a $50bn market cap, their stock performance suffers,” Nuttall told shareholders last year. “When you have a lot of people, you get siloed. People start working not for the overall firm, but maybe for the group they’re in. Risk management suffers,” he added.

But in the event of a sharp downturn, KKR would have to write down the value of its subsidiary investments just like any other company. In April, when markets were rocked by the announcement of President Donald Trump’s “reciprocal” tariffs, KKR’s shares fell more than those of Blackstone — a sign of investors’ wariness.

“The concerns for Apollo and KKR have been around the negative earnings revisions around the insurance side of the operation,” says Katz, at TD Cowen. “For Blackstone, it is more about the fees they earn from realisation activity,” he adds, referring to the sales of assets that generate profits for investors and performance fees for Blackstone.

During the pandemic, Blackstone raised by far the most money of any private capital group on Wall Street, taking in nearly $270bn during 2021 alone.

The fundraising, likened by Schwarzman at the time to an “out of body experience”, was the reward for hiring hundreds of new salespeople to distribute Blackstone funds to wealthy individual investors in preceding years.

Executives believed this market could expand for decades, in time potentially becoming larger than the pension funds and endowments that had fuelled Blackstone’s initial growth.

The group’s assets and fee income outpaced those of its rivals as it put the cash to work. At one point, its market value was far greater than that of its two largest rivals combined, with Schwarzman receiving dividends of over $1bn in 2021.

Blackstone’s funds, such as its flagship evergreen property vehicle, Breit, promised investors large dividends. As the money flooded in during a decade of ultra-low interest rates, it had to be quickly recycled into assets, even if that carried the risk of overpaying.

Once interest rates began to rise rapidly in 2022, investors in Breit began to pull their cash out. Blackstone was forced to limit investor withdrawals to avert being forced to sell assets, and after a year-long campaign to calm their frightened investors, Schwarzman and Gray eventually stabilised Breit.

But the challenges were a reminder of the risks. “You can be the best real estate investor in the world — but if you take $50bn and invest it all on Tuesday in one interest rate environment, and rates go up, then everything you own is underwater,” says a top executive at another large private equity group. “Their sin was a sin of growth.”

Blackstone describes this as “a false premise”, noting that since the start of 2022 Breit has “materially outpaced” both publicly traded property funds and private real estate.

The head of another group says the Blackstone model is the one most susceptible to any change in public perceptions of its investment skill and its overall returns. “But their ballast is that they have invested in distribution. They are asset light, but they’ve built a distribution engine that can sell products better than anyone else on Wall Street.”

The contrasting business models of the private capital industry’s three titans will set the tone of the industry in the decades to come, as rivals such as EQT and CVC Capital in Europe and Blue Owl and TPG in the US decide which approach to adopt.

BlackRock, the world’s largest asset manager, has also signalled its intention to expand in private markets and will face decisions about how to fund its growth.

An early indicator of the direction of travel could be the fate of Brighthouse, an insurer with $120bn in investments that put itself up for sale this year. It has received interest from several large private capital groups including TPG, Carlyle Group and Sixth Street.

For a group like TPG, any acquisition would suggest a move towards Apollo’s model, while remaining on the sidelines may indicate a preference for Blackstone’s approach of simply managing third-party assets.

“There are merits to both models and risks to both models,” says a top adviser to private capital groups. “Blackstone’s policy is a more conservative one. But is it overly conservative? Are they worrying too much about the black box risk in the insurance liabilities?”

Cyprys, at Morgan Stanley, also notes that the divergent strategies have yet to be tested by a prolonged recession or a sustained market crisis.

“There is still a question on how those business models will perform through a more meaningful downturn that we haven’t seen in many, many years,” he says.