Trump’s aggressive push to roll back globalisation

In 1987, Donald Trump took out a full-page advert in The New York Times and other papers to complain about how the global system was stacked against the US.

In an open letter that still defines his worldview, the 41-year-old property developer objected to the impact of a strong dollar on manufacturing, Japan’s trade surplus and the cost of military aid for allies. “End our huge deficits, reduce our taxes, and let our economy grow,” he wrote.

Nearly four decades later and emboldened by his popular vote victory in November’s election, Trump feels he is finally in a position to enact that agenda and try to reverse the course of economic history.

For all the absurdities of Trump’s “liberation day” speech — from the giant blue cards outlining the new tariffs to the bogus formula littered with Greek letters that was used to justify the figures — the announcement is a distillation of the core impulses about trade he has long held.

The extent of the rupture cannot be overstated: Trump wants to unwind the multi-decade process of integrating the global economy.

To much of the rest of the world, the global trading system helped America become the most prosperous and successful nation in history. But for Trump, the US is a victim.

For the past five decades, as the president claimed on Wednesday in the Rose Garden, his country has been “looted, pillaged, raped and plundered” by friends and foes alike. “Now it is our turn to prosper.”

Some investors had been operating under the assumption that Trump was bluffing about tariffs. But since Thursday, markets have seen frenzied selling driven by a sense that reckless US economic policymaking risks driving the economy into recession and crippling global growth.

“It looks like a good old-fashioned market panic,” said Andrew Pease, chief investment strategist at Russell Investments, on Friday as global equities plunged for a second consecutive day.

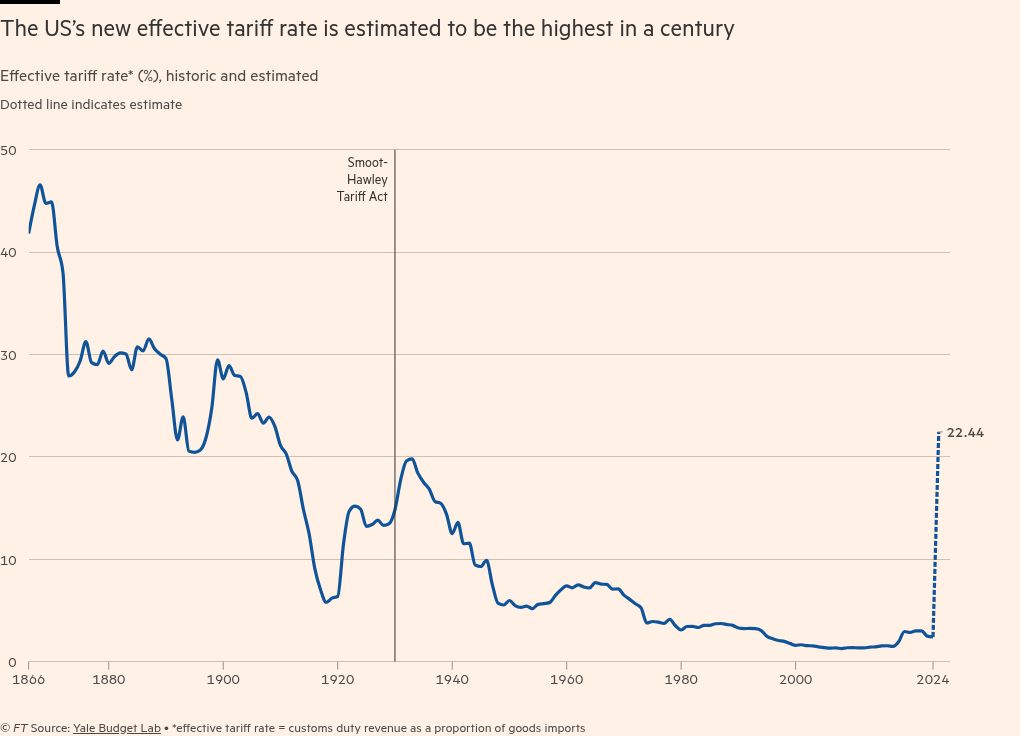

The tariff onslaught Trump announced on Wednesday would — if fully enacted — in some ways take the global trading system back a century or more, pushing the average effective tariff on US imports to its highest rate since 1909 according The Budget Lab, a research organisation.

The complacency about Trump’s plans has been replaced by a series of urgent questions. What sort of global economy does Trump actually want to see? Is there a genuine plan beyond the bombast and victim rhetoric? Will he back down? And how grave are the global economic and political consequences of his gambit?

Trump’s ire is often focused on the period of rapid globalisation that started in the late 1980s and was fuelled by China’s accession to the WTO in 2001. At times, he appears to wish to restore the US to the sort of economic primacy it enjoyed during his childhood in the 1950s, before Germany, Japan or later China began to seriously challenge America’s position as the factory of the world.

But Gary Richardson, a professor of economic history at the University of California at Irvine, says the policies Trump championed on Wednesday bear clearer similarities to those of America in the 19th century, when tariffs rather than income taxes were the main source of government revenue.

Others liken the threat now hanging over the global economy to the 1930s, when the infamous Smoot-Hawley tariffs in the US set off a chain reaction of international retaliation, often blamed for deepening the Depression.

In some ways the current risks could be greater. Not only is trade more important than it was in the 1930s, but today’s global economy is built on intricate supply chains that see goods and parts flow across multiple borders — all sustained by a framework of international co-operation that Trump is spurning.

“It is just a huge gamble, and the historical analogies suggest things could go really, really wrong,” says Richardson, who specialises in the Depression and Federal Reserve history. “It is kind of scary.”

In his assault on globalisation, Trump has been pushing on a door that was already ajar. The loss of manufacturing jobs to Mexico, China and other less developed countries and the global financial crisis had damaged public confidence in postwar economic orthodoxy.

The rise of China shifted political opinion, too. If Beijing was potentially a peer geopolitical rival to Washington, maybe it made strategic sense for the US to seek to slow China’s rampaging economic growth — a policy pursued avidly during former president Joe Biden’s four years in the White House.

Trump has fused these resentments about trade with his own psychology. The globalisation era was defined by the idea of win-win — that both sides can benefit from compromise. But Trump, shaped by his experience as a real estate developer bidding for plots of land, believes there can only be one winner in a negotiation. He prides himself in never backing down or showing weakness.

“We are seeing a combination of true-believing mercantilism, shocking ignorance about how the global economy works, and shocking incompetence in the planning and execution of economic policy,” says Michael Strain of the conservative American Enterprise Institute.

If there is a unifying theory of the case behind Trump’s tariffs, parts of it can be found in a widely read paper from last November by Stephen Miran, now the chair of Trump’s Council of Economic Advisers, which outlines how tariffs might be used to boost American manufacturing.

Miran’s argument is nuanced, acknowledging that there is little prospect of restoring jobs in low-value added industries such as textiles. But he believes tariffs could bring advantages to high-end manufacturing in the US and could prevent further offshoring.

He also speaks of the need to avoid tariffs driving up an already strong dollar and undermining US competitiveness, positing ideas for coercing allies into co-operating on currency policy that have been widely criticised.

Trump himself has been vague about what sort of jobs he really thinks can be brought back to the country, despite occasional comments about the importance of making steel or cars. And as most economists have been quick to point out this week, there are myriad problems with the Trump team’s arguments.

The stated objectives are often contradictory. At times, tariffs are presented as a tool to reshape the economy and bring back manufacturing, but at others they are a way to gain diplomatic leverage. The economic goal of tariffs can be to raise revenue from imports or it can be to shrink imports by increasing domestic production — but it cannot be both.

The White House strategy appears to underestimate the vital role that foreign products serve as inputs into US manufacturing, although Trump’s decision to exempt Mexico and Canada from his across-the-board 10 per cent baseline tariff suggests some belated recognition of this reality.

Trump’s speech also completely ignored the services sector, which makes up around 70 per cent of the US economy. And many of the tariffs baldly contradict national security priorities: for example the US wants to challenge China, but is clobbering Japan, a key ally, with a 24 per cent levy.

The problem terrifying global investors is the risk of a 1930s-style race to erect barriers that destabilises the global economy and undermines global co-operation.

Trump on Wednesday offered a revisionist view of that period, proposing the novel argument that the Depression would never have happened if the US had kept in place a tariff-based system rather than shifting decades earlier to income tax.

Scott Bessent, the US Treasury secretary, appeared to acknowledge the dangers of tit-for-tat retaliation to the tariffs, urging countries to “sit back, take it in, and let’s see how it goes”.

Strain argues that Trump has left open a route to easing the top-up tariffs, with the baseline 10 per cent levy likely to be permanent while the administration does deals on the additional elements, which are due to take effect on April 9. Trump has suggested he is open to cutting tariffs in return for “phenomenal” offers.

China announced its own 34 per cent tariffs on US goods on Friday. However, the initial response of the EU and UK has been to reject immediate retaliation, in the hopes that Trump can be convinced to water down the measures.

That may be a forlorn hope. This is also an administration that in a short period of time has gone out of its way to antagonise major trading partners — from Trump’s threats to annex Canada and Greenland to vice-president JD Vance’s speech to the Munich Security Conference, when he accused European leaders of backsliding on democracy and freedom of speech.

While Trump appears to be less cowed by adverse movements in financial markets than in his first term, the White House will find it difficult to ignore the investor revolt against its policies. Recession warnings have begun to proliferate in recent days as economists digest the prospective lurch in the US tariff rate to around 22 per cent, from just 2.5 per cent last year.

History suggests that once imposed, tariffs are politically difficult to remove. Trump’s announcements mark “a clean break with the trade policy of the last 60 or more years . . . we are back in the interwar environment [of protectionism],” says Kris Mitchener, a professor at Santa Clara University. “It could trigger other countries to retreat to retaliation.”

Economists warn trade conflicts like those in the 1930s can be highly perilous, not just for economies but in driving a wider breakdown in co-operation that infects broad swaths of international policy.

“Trade war is costly,” says Kirsten Wandschneider, an economic historian at Vienna university, who argues that the US suffered more than previously thought from the boycotts, quotas and tariffs other countries put in place in response to the Smoot-Hawley measures. “Retaliation is something that should not be underestimated.”

Richardson, the historian of the Depression, cautions that serious disputes over trade can spill into wider global politics, fostering tensions that can even lead to wars. “We could see international co-operation decline across many dimensions,” he says.

“There is a lot of other stuff that can go off the rails.”

Additional reporting by Ian Smith in London